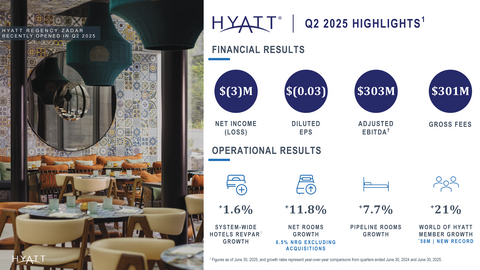

- Comparable system-wide hotels RevPAR increased 1.6%, compared to the second quarter of 2024

- Net rooms growth was 11.8% and net rooms growth excluding acquisitions was 6.5%

- Net Income (loss) attributable to Hyatt Hotels Corporation was $(3) million and Adjusted Net Income was $66 million

- Diluted EPS was $(0.03) and Adjusted Diluted EPS was $0.68

- Gross fees were $301 million, an increase of 9.5%, compared to the second quarter of 2024

- Adjusted EBITDA was $303 million, a decrease of 1.1%, compared to the second quarter of 2024, or an increase of 9.0% after adjusting for assets sold in 2024

- Pipeline of executed management or franchise contracts was approximately 140,000 rooms, an increase of approximately 8%, compared to the second quarter of 2024

- Full Year 2025 Outlook: The following metrics do not include the impact of the Playa Hotels Acquisition and the pending Playa Real Estate Transaction. Refer to page 3 and the tables beginning on schedule A-11 for the impact of Playa on full year outlook.

- Comparable system-wide hotels RevPAR growth is projected between 1% to 3%, compared to the full year 2024

- Net rooms growth excluding acquisitions is projected between 6% to 7%, compared to the full year 2024

- Net income is projected between $135 million and $165 million

- Adjusted EBITDA is projected between $1,085 million and $1,130 million, an increase of 7% to 11% after adjusting for assets sold in 2024, compared to the full year 2024

- Capital Returns to Shareholders is projected to be approximately $300 million, through a combination of dividends and share repurchases

Mark S. Hoplamazian, President and Chief Executive Officer of Hyatt, said, “The second quarter’s results reflect solid performance across our business, including strong fee contribution in a lower RevPAR growth environment. As we look ahead, we are encouraged by recent booking trends, leaving us optimistic about improving performance in the fourth quarter and into next year. We are confident that we will continue to deliver strong financial results as we leverage our brand-led strategy and long history of industry leading net rooms growth.”

Mr. Hoplamazian continued, "The Playa transactions, including the agreement to sell the entirety of Playa’s real estate portfolio, reinforce our commitment to our asset-light business model and solidifies our leadership in the fast-growing luxury all-inclusive segment. The acquisition and planned disposition of the Playa real estate portfolio, at an attractive multiple, allows us to once again create highly durable fees and long term value for shareholders.”

Second Quarter Operational Commentary

- Luxury chain scales drove RevPAR growth in the second quarter, while select service hotels in the United States saw RevPAR decline compared to the second quarter of 2024. RevPAR growth was negatively impacted by 60 bps due to the timing of the Easter holiday in the second quarter, which fell in the first quarter last year.

- Gross fees increased 10% in the quarter, compared to the second quarter last year, with properties from the Bahia Principe and Standard International Transactions contributing approximately $11 million, or approximately 42% of the total gross fees growth.

- Base management fees: increased 13%, driven by managed hotel RevPAR growth and the contribution of newly-opened hotels.

- Incentive management fees: grew 15%, led by newly-opened hotels, all-inclusive resorts performance, United States resorts, and favorable foreign currency exchange rates.

- Franchise and other fees: expanded 4%, due to non-RevPAR fee contributions and newly-opened hotels.

- Owned and leased segment Adjusted EBITDA increased 1%, compared to the second quarter of 2024, after adjusting for assets sold in 2024 and the impact of the Playa Hotels Acquisition. Comparable owned and leased margin decreased by 170 bps in the second quarter, compared to the same period in 2024.

- Distribution segment Adjusted EBITDA was flat, compared to the second quarter of 2024, as higher pricing, effective cost management, and favorable foreign currency exchange offset lower booking volumes.

Openings and Development

During the second quarter, the Company:

- Opened 8,920 rooms, inclusive of approximately 2,600 rooms associated with the Playa Hotels Acquisition. Notable openings included:

- Hyatt Regency Zadar, Hyatt's first property in Croatia; Dreams Rose Hall Resort & Spa; Zélia Halkidiki, a Destination by Hyatt hotel; and AluaSoul Sunny Beach.

- Announced a new upscale brand, Unscripted by Hyatt, which is designed to unlock growth through adaptive reuse and conversion-friendly opportunities, giving owners a flexible path to benefit from our global distribution and World of Hyatt loyalty program.

Transactions

The Company has provided the following updates on the Playa Hotels Acquisition and Playa Real Estate Transaction:

- Announced the completion of the Playa Hotels Acquisition for $2.6 billion on June 17, 2025.

- Announced entry into a definitive agreement with Tortuga Resorts, a joint venture between an affiliate of KSL Capital Partners, LLC and Rodina, to sell the entirety of the real estate portfolio acquired as part of the Playa Hotels Acquisition for $2.0 billion on June 30, 2025. Concurrent with the sale, which is expected to close before the end of 2025, the Company will enter into 50-year management agreements for 13 of the 15 resorts.

- The Company is required to use the proceeds from the Playa Real Estate Transaction to repay the $1.7 billion delayed draw term loan used to fund a portion of the Playa Hotels Acquisition.

Balance Sheet and Liquidity

As of June 30, 2025, the Company reported the following:

- Total debt of $6.0 billion, inclusive of the $1.7 billion delayed draw term loan facility.

- Total liquidity of $2.4 billion, inclusive of:

- $912 million of cash and cash equivalents, and short-term investments, and

- $1,497 million of borrowing capacity under Hyatt's revolving credit facility, net of letters of credit outstanding.

- Total remaining share repurchase authorization of $822 million. The Company did not repurchase any shares of Class A common stock during the second quarter.

2025 Outlook

2025 Full Year Outlook, excluding the impact of the Playa Hotels Acquisition and Playa Real Estate Transaction | ||||||

|

| 2025 Outlook |

| 2024 Reported |

| Growth vs 2024 |

System-Wide Hotels RevPAR Growth |

|

|

|

|

| 1% to 3% |

Net Rooms Growth |

|

|

|

|

| 6% to 7% |

(in millions) |

|

|

|

|

|

|

Net Income |

| $135 - $165 |

| $1,296 |

| (90)% to (87)% |

Gross Fees |

| $1,195 - $1,215 |

| $1,099 |

| 9% to 11% |

Adjusted G&A Expenses1 |

| $450 - $460 |

| $444 |

| 1% to 4% |

Adjusted EBITDA1 |

| $1,085 - $1,130 |

| $1,0162 |

| 7% to 11%2 |

Capital Expenditures |

| Approx. $150 |

| $170 |

| Approx. (12)% |

Adjusted Free Cash Flow1 |

| $450 - $500 |

| $540 |

| (17)% to (7)% |

Capital Returns to Shareholders3 |

| Approx. $300 |

|

|

|

|

1 Refer to the tables on schedule A-11 for a reconciliation of estimated net income (loss) attributable to Hyatt Hotels Corporation to Adjusted EBITDA, G&A expenses to Adjusted G&A Expenses, and net cash provided by operating activities to Free Cash Flow and Adjusted Free Cash Flow.

2 Reflects a reduction of $80 million to 2024 owned and leased segment Adjusted EBITDA to account for the impact of sold hotels. Refer to schedule A-10 for further details.

3 The Company expects to return capital to shareholders through a combination of cash dividends on its common stock and share repurchases.

- System-wide RevPAR outlook implies balance of year growth of 0% at the low end of our range and 2% at the high end of our range, and reflects a continuation of trends seen in the second quarter into the third quarter while anticipating an improvement in the United States during the fourth quarter.

- Net income outlook projected year over year decline is driven by 2024 gains on sale of real estate and other.

- Adjusted EBITDA outlook is projected between $1,085 million - $1,130 million, growing between 7% to 11% compared to the full year 2024 after adjusting for assets sold in 2024.

- Adjusted Free Cash Flow growth compared to full year 2024 is impacted by elevated levels of interest expense and cash taxes.

- The Company has reinstated its 2025 outlook for capital returns to shareholders, and is projected to return approximately $300 million of capital to shareholders through a combination of cash dividends on its common stock and share repurchases.

2025 Full Year Outlook, including the impact of the Playa Hotels Acquisition | ||||||

|

| Hyatt (Ex-Playa) |

| Playa4 |

| Consolidated |

System-Wide Hotels RevPAR Growth |

| 1% to 3% |

| —% |

| 1% to 3% |

Net Rooms Growth |

| 6% to 7% |

| 0.7% |

| 6.7% to 7.7% |

(in millions) |

|

|

|

|

|

|

Net Income |

| $135 - $165 |

| $(113) - $(112) |

| $22 - $53 |

Gross Fees |

| $1,195 - $1,215 |

| Approx. $(5) |

| $1,190 - $1,210 |

Adjusted G&A Expenses5 |

| $450 - $460 |

| $4 - $6 |

| $454 - $466 |

Adjusted EBITDA5 |

| $1,085 - $1,130 |

| $70 - $85 |

| $1,155 - $1,215 |

Capital Expenditures |

| Approx. $150 |

| $65 |

| Approx. $215 |

Adjusted Free Cash Flow5 |

| $450 - $500 |

| $(15) |

| $435 - $485 |

Capital Returns to Shareholders6 |

| Approx. $300 |

| $— |

| Approx. $300 |

4 Assumes the Playa Real Estate Transaction does not close before December 31, 2025 and that the real estate acquired as part of the Playa Hotels Acquisition is held through December 31, 2025. Transaction costs and other expenses associated with the Playa Real Estate Transaction are included for 2025 Adjusted Free Cash Flow and Net Income.

5 Refer to the tables beginning on schedule A-11 for a reconciliation of estimated net income (loss) attributable to Hyatt Hotels Corporation to Adjusted EBITDA, G&A expenses to Adjusted G&A Expenses, and net cash provided by operating activities to Free Cash Flow and Adjusted Free Cash Flow.

6 The Company expects to return capital to shareholders through a combination of cash dividends on its common stock and share repurchases.

Other than with respect to the Playa Hotels Acquisition, as noted above, no disposition or acquisition activity beyond what has been completed as of the date of this release has been included in the 2025 Outlook. The Company's 2025 Outlook is based on a number of assumptions that are subject to change and many of which are outside the control of the Company. If actual results vary from these assumptions, the Company's expectations may change. There can be no assurance that Hyatt will achieve these results.

Refer to the table on schedule A-9 for a summary of special items impacting Adjusted Net Income and Adjusted Diluted EPS for the three and six months ended June 30, 2025.

Note: All RevPAR and ADR growth percentage changes are in constant dollars. All Net Package RevPAR and Net Package ADR growth percentage changes are in reported dollars. This release includes references to non-GAAP financial measures. Refer to the non-GAAP reconciliations included in the schedules and the definitions of the non-GAAP measures presented beginning on schedule A-6.

Conference Call Information

The Company will hold an investor conference call this morning, August 7, 2025, at 9:00 a.m. CT.

Participants may listen to a simultaneous webcast of the conference call, which may be accessed through the Company's website at investors.hyatt.com. Alternatively, participants may access the live call by dialing: 800.715.9871 (U.S. Toll-Free) or 646.307.1963 (International Toll Number) using conference ID# 2303828 approximately 15 minutes prior to the scheduled start time.

A replay of the call will be available Thursday, August 7, 2025 at 12:00 p.m. CT until Thursday, August 14, 2025 at 10:59 p.m. CT by dialing: 800.770.2030 (U.S. Toll-Free) or 647.362.9199 (International Toll Number) using conference ID# 2303828. An archive of the webcast will be available on the Company's website for 90 days.

Investor Contacts

- Adam Rohman, 312.780.5834, adam.rohman@hyatt.com

- Ryan Nuckols, 312.780.5784, ryan.nuckols@hyatt.com